Over the last year we have received numerous questions regarding the new administration’s impact on the Washington region, and particularly, the office market. More recently, concerns about the effect of AI on the office market have bubbled to the surface. So, we thought we would get AI’s view on the topic. In this case, a perspective courtesy of Google Gemini.

![]() Predictions for AI’s impact on the office leasing market through 2026 suggest a dual effect: it is currently a “lifeline” for major tech hubs like San Francisco but poses a long-term “headwind” for overall demand due to automation.

Predictions for AI’s impact on the office leasing market through 2026 suggest a dual effect: it is currently a “lifeline” for major tech hubs like San Francisco but poses a long-term “headwind” for overall demand due to automation.

Key Market Trends (2025–2026)

- Selective Rebound: AI is fueling a “flight to quality,” where demand concentrates in top-tier “Trophy” assets in cities like New York, San Francisco, Seattle, Boston

- Market Bifurcation: High-quality buildings in prime locations are seeing dropping vacancies (e.g., Midtown Manhattan), while “commodity” or older buildings in non-prime locations face higher risks of obsolescence as AI automates the back-office roles that traditionally occupied them.

- Growth in Lease Size: As AI firms mature, they are scaling from small requirements (3,000–5,000 sq. ft.) to significantly larger footprints (15,000–20,000+ sq. ft.).

Long-Term Projections (Through 2030)

- Stagnant Employment Growth: Real estate firms like Newmark project that office-using employment growth will remain essentially flat (+0.3%) between 2026 and 2030 as AI productivity gains offset the need for new hires.

- Vacancy Forecasts:

- Base Case: National vacancy is expected to reach 21.5% by 2030.

- Severe Downside: If AI causes significant job displacement without creation, vacancy could hit a record 23.5%.

- Space Evolution: Future offices will likely focus less on “desks for tasks” and more on “hubs for high-value collaboration,” requiring redesigned floorplans with lower desk density and more meeting spaces.

1. Industrial Real Estate: High-Tech Efficiency

The industrial sector is moving from “static” storage to “strategic” fulfillment.

- Predictive Logistics: AI reduces “exception costs” (rushed shipments) by predicting local demand spikes, allowing inventory to be repositioned before sales occur.

- Automation Premium: Buildings designed for advanced robotics command a 10% rental premium because they offer higher throughput and lower labor intensity.

- Micro-Fulfillment: Growth is shifting toward smaller, urban “last-mile” centers that prioritize speed over scale, often using AI-driven drone or autonomous delivery models.

2. Retail Real Estate: Experience over Inventory

Physical retail is pivoting toward “immersive environments” that digital transactions cannot replicate.

- Store as Showroom: AI-driven “fit tools” and virtual try-ons reduce in-store stock requirements, allowing retailers to repurpose space for storytelling and entertainment.

- Frictionless Checkout: In high-footfall urban areas, AI computer vision (similar to Amazon Go) is making smaller, expensive sites viable by processing more transactions per hour with less staff.

- Predictive Specialization: Retailers are using AI to specialize store formats based on local demographics rather than using “cookie-cutter” designs across all locations.

3. Multifamily Real Estate: Autonomous Management

Multifamily is entering an era of “autonomous property management” aimed at increasing Net Operating Income (NOI).

- Leasing Automation: AI assistants now handle the entire “Search-to-Sofa” journey—scheduling tours, verifying identities, and processing leases 24/7. Firms using these tools report up to an 80% decrease in time spent on renewals.

- Predictive Maintenance: IoT sensors combined with AI can predict HVAC or plumbing failures before they occur, potentially reducing maintenance costs by up to 25%.

- Resident Retention: Sentiment analysis tools monitor tenant reviews and maintenance requests to flag “at-risk” residents before they decide to move out, improving retention rates by nearly 20%.

Real Estate Impact Summary (2025–2030)

| Product Type | Core AI Impact | Key Economic Metric |

|---|---|---|

| Industrial | Autonomous robotics & predictive inventory | 10% rent premium for automated hubs |

| Retail | Experiential showrooms & frictionless checkout | Reduced stock-holding; higher sales/sq ft |

| Multifamily | Automated leasing & predictive maintenance | 8–12% average NOI improvement |

Thank you Gemini for this summary of AI impacts.

There is a lot to think about here, threads to follow and certainly opportunities to go deeper. Gemini’s predictions for the office market are certainly somber, but it stops short of predicting negative job growth over the next five years. With significant conversion activity taking place, even with flat job growth, it would follow that office vacancy rates should fall over time. This dynamic is what we are seeing in the DC region – flat absorption of space, very little new supply coming on-line and falling inventory due to the conversion of obsolescent office buildings to other uses. In particular, we are seeing this show up in the Class A and trophy office space where vacancy rates have dropped almost 700 basis points over the last two years and rents have grown 7% year-over-year.

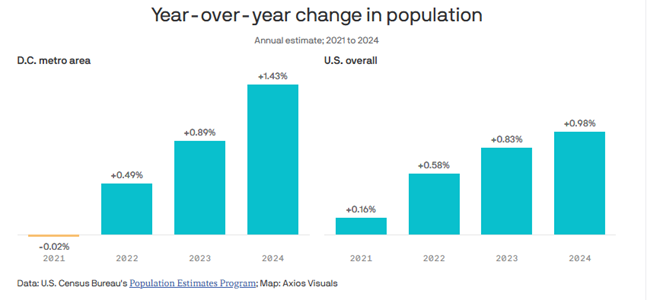

Region-wide, we are still seeing and feeling the effects of recent government downsizing, particularly in parts of downtown Washington where there has been an increase in retail and restaurant vacancy along with high vacancy in office buildings. However, there are signs of economic stabilization across the region. From mid-2024 to mid-2025, the Washington MSA was the seventh fastest growing region in the country, demonstrating the resilience of the region and its continued diversification away from dependence on the federal government.

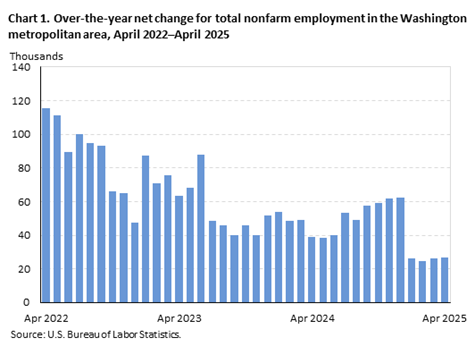

This diversification is evident in the region’s labor market, as well. Despite some of the challenges faced in DC, the region continued to add jobs, albeit at a level below the historical average. The accompanying chart reflects the sudden drop in employment at the beginning of last year with the initial government efficiency efforts of DOGE, and early retirements and RIFs of government employees. Notwithstanding these initiatives, the region had overall positive job growth.

We have been writing about the market bottoming for several quarters, and we believe it will be a long bottom due to the tepid growth rate of the local economy, and the continued clean-up of underwater properties. It is, and will continue to be, however, a market that will provide opportunities where buyers see future value to be created in properties that sellers see as deeply troubled. As one highly respected market participant recently said, “This is the best time to buy office in my career.” When pressed about the malaise of the office market he responded, “I am not buying office to keep it as office. There are many conversion options available to the creative mind if one can buy at the right price.”

![]() “Well said, Human.”

“Well said, Human.”